{kind=link}

{kind=link}

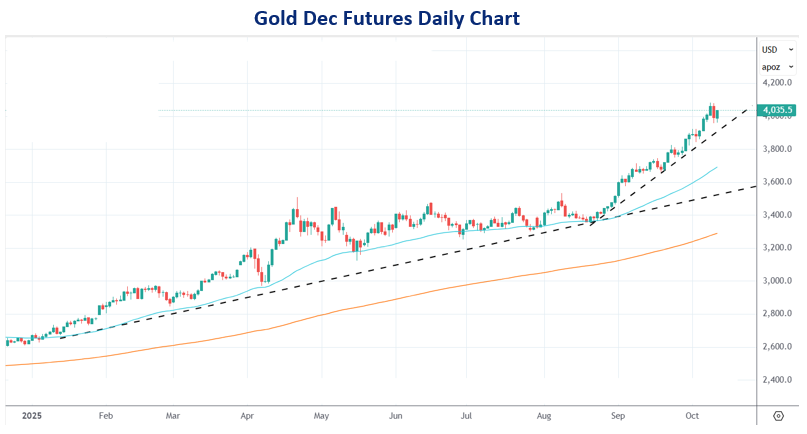

With a 3% weekly gain and a 52% annual gain, gold prices have risen for the eighth consecutive week due to concerns about the global economy, persistent geopolitical unpredictability, and growing anticipation of additional US interest rate cuts. Last week, spot gold jumped beyond the $4000 psychological barrier, driven by heightened tensions between Washington and Beijing after US President Trump said there was no reason to meet with China’s Xi Jinping in South Korea as scheduled in two weeks and that he was ready to raise duties on Chinese imports by 100%.

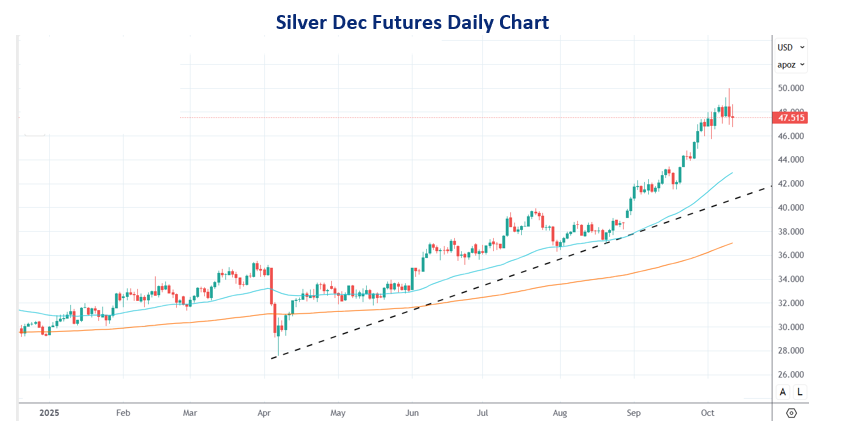

With a record high of $50 and its eighth consecutive weekly gain, silver prices have increased by around 75% this year due to strong demand for safe-haven assets and ongoing supply bottlenecks. Frequent backwardation, in which spot prices surpass futures, prolonged physical deficits, and depleted inventory are all hallmarks of stress in the global silver market. Such tightness has historically resulted in higher spot prices, as demonstrated by the 2010–11 rally, when silver rose to $50/oz.

That incident is mirrored in the 2025 setup: high industrial demand, particularly from solar, multi-year supply shortages, and tightening visible stocks. However, geopolitical risk and global monetary easing are also driving the current rise, unlike in 2011. Silver may remain high if deficits continue, but volatility risk is still considerable. Demand has also increased as a result of political unpredictability, such as the US government shutdown, upheaval in France, and changes in Japanese leadership. Prices are under further pressure to rise due to a lack of easily accessible silver in the London market.

Safehaven purchasing in precious metal packs should preferably be put on hold as Israel’s government confirmed a ceasefire with Hamas on Friday, moving the conflict in Gaza to a 24-hour standstill.

This year’s gold rally is an indication of growing mistrust of the current monetary and fiscal system. The U.S., U.K., France, and Japan are the four largest economies with debt loads over 100% of their respective GDPs, and their fiscal profiles continue to deteriorate. The Swiss franc and the yen, two other conventional safe-haven assets, are also becoming less attractive.

Geopolitical risks are still high, central banks are still purchasing, Trump’s trade war is still ongoing, and ETF holdings are still growing as the likelihood of further Fed rate cuts increases. Gold’s surge currently has a FOMO (fear of missing out) component. However, the foundations that have propelled it thus far are still very much in place.

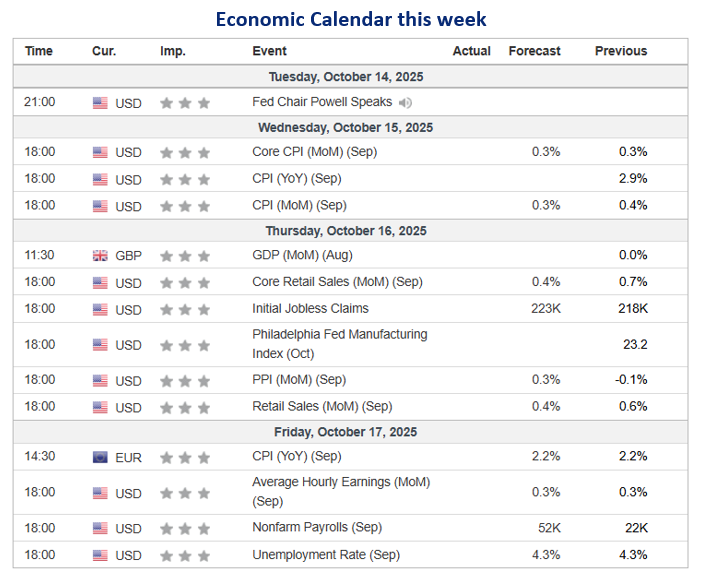

Moreover, we will not get the CPI release on Wednesday if the shutdown continues into this week, which will make us more and more unsure about the state of the American economy.

Gold has achieved all targets at $4000 (~Rs 120,000). As this runup continues, the next resistance is $4150 (~Rs 125,000). One needs to be very cautious at this level. However, if Gold futures sustain below last Thursday’s low of $3958 (~Rs 120,000), we can say that, short-term top has been made, and a correction will follow for at least 4-5%.

Silver has achieved the target of $50 (~Rs 150,000). If Silver prices sustain above this level, the next target is $55 (~Rs 165,000). However, last week’s Thursday low of $46.70 (~Rs 144,000) is a very strong support. If Silver futures sustain below this level, we could see more correction or profit booking by at least 4-5%.

Disclaimer: This report contains the opinion of the author, which is not to be construed as investment advice. The author, Directors, and other employees of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd. and its affiliates cannot be held responsible for the accuracy of the information presented herein or for the results of the positions taken based on the opinions expressed above. The above-mentioned opinions are based on information which is believed to be accurate, and no assurance can be given of the accuracy of the information. The author, directors, other employees and any affiliates of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd cannot be held responsible for any losses in trading. In no event should the content of this research report be construed as an express or implied promise, guarantee or implication by or from Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd., that the reader or client will profit, or the losses can or will be limited in any manner whatsoever. Past results are no indication of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. The information contained in this report is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. We do not offer any sort of portfolio advisory, portfolio management or investment advisory services. The reports are only for information purposes and are not to be construed as investment advice.