{kind=link}

{kind=link}

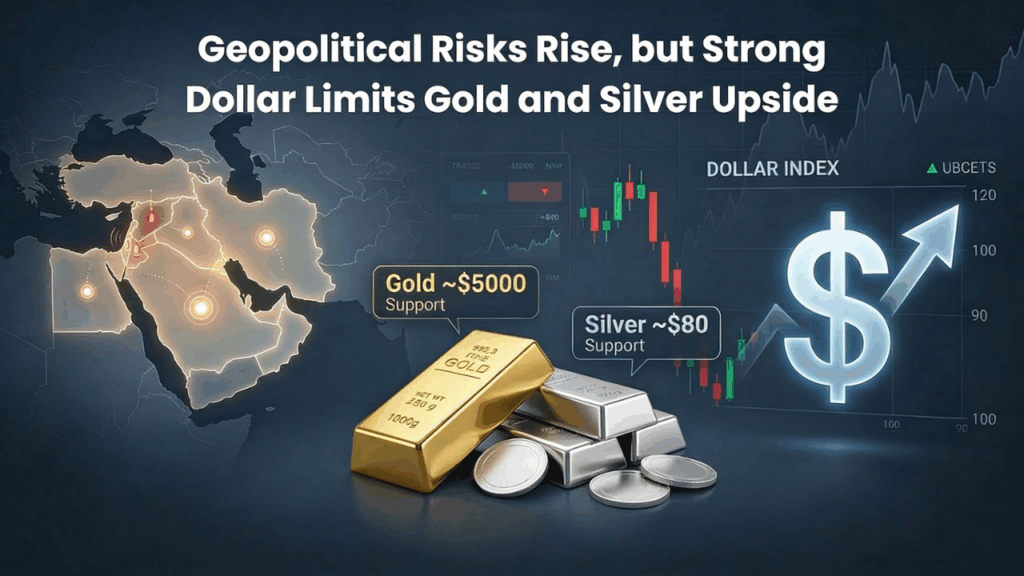

Gold prices have established support at approximately $5000, while silver has stabilized near the $80 mark. These levels represent critical support zones amid volatile market conditions driven by competing economic narratives.

Currency Strength and Safe-Haven Positioning

The U.S. dollar has strengthened substantially, breaking above the 100 index level. This appreciation reflects investor preference for dollar-denominated assets as geopolitical uncertainty intensifies in the Middle East. The greenback’s strength can be attributed to two primary factors:

- Energy Independence Advantage: The U.S. maintains structural advantages as a net crude exporter, positioning it more favorably than other developed economies heavily dependent on imported oil.

- Geopolitical Risk Premium: Recent military escalation, including the largest U.S. military strikes against Iranian targets and continued blockade of the Strait of Hormuz, has reinforced the dollar’s safe-haven status.

Macroeconomic Constraints on Precious Metals

-

Economic Growth Slowdown

Recent data revisions indicate Q4 2025 annualized GDP growth decelerated to 0.7%, introducing genuine concerns regarding economic momentum. This slowdown conflicts with traditional precious metals demand narratives and undermines the typical inverse relationship between economic growth and precious metals investment.

-

Inflation and Monetary Policy Expectations

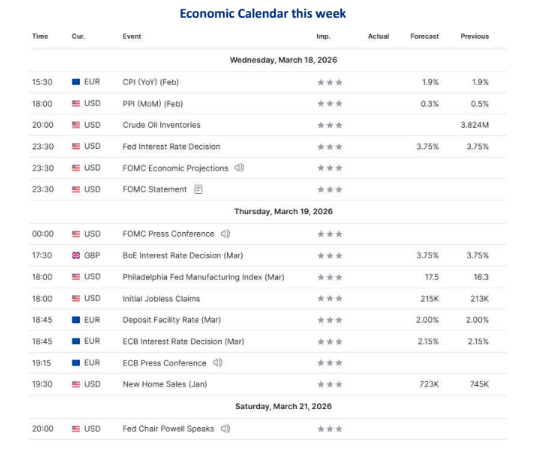

The Personal Consumption Expenditures (PCE) inflation rate has moderated to 2.8% annually, yet crude oil prices exceeding $100 per barrel threaten to reverse disinflationary momentum. The Federal Reserve has postponed anticipated interest rate cuts to September 2026, a significant shift that disadvantages non-yielding assets such as precious metals and gold.

Oil Price Dynamics and Regional Economic Impact

-

Inflationary Pressures from Energy Markets

Crude oil prices climbing above $100 per barrel present a dual challenge: they sustain inflation concerns while simultaneously supporting dollar strength as investors seek U.S. assets. Market participants have effectively eliminated expectations for multiple Federal Reserve rate cuts in 2026, recognizing the inflationary implications of elevated oil prices.

-

Asymmetric Economic Exposure

The geopolitical conflict between the U.S. and Iran creates asymmetric economic consequences:

- Vulnerable economies: Japan and the eurozone face severe economic headwinds due to heavy reliance on crude imports

- Insulated markets: The United States maintains relative insulation, having functioned as a net crude exporter for nearly a decade

Policy interventions, including President Trump’s partial 30-day waiver on sanctioned Russian oil purchases, represent attempts to moderate price escalation, though effectiveness remains uncertain.

Physical Markets and Retail Demand Deterioration

-

Indian Bullion Market Dynamics

Indian bullion dealers have extended discount offerings to unprecedented levels, reaching $83 per ounce over domestic official pricing (inclusive of 6% import and 3% sales levies)—the highest discount observed since July 2016, compared to $28 the previous week. This dramatic expansion in dealer discounts reflects profound weakening in retail demand.

-

Jewelry Sector Weakness

The jewelry sector exhibits particular vulnerability, with jewelers demonstrating minimal purchasing activity as they prioritize year-end financial accounting. Weak retail demand transmission throughout distribution channels suggests limited near-term support for precious metals prices at current levels.

The convergence of dollar strength, delayed rate-cut expectations, elevated oil prices, and weakening physical demand creates a challenging environment for precious metals. While geopolitical instability typically supports precious metals valuations, the current macroeconomic framework—characterized by economic deceleration, monetary policy tightening bias, and currency appreciation—has effectively neutralized traditional safe-haven appeal in favor of dollar accumulation and higher-yielding alternatives.

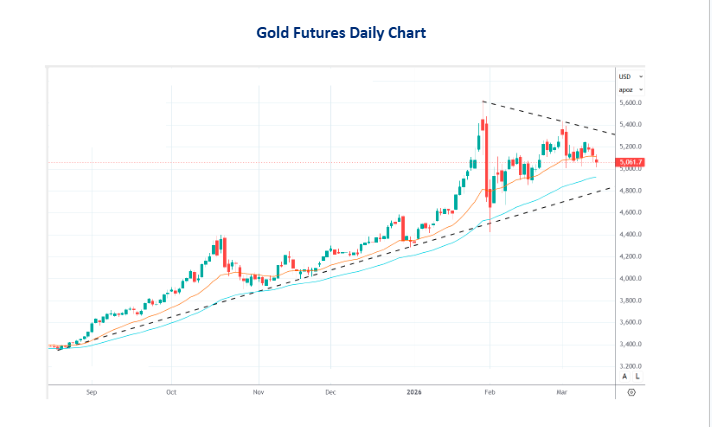

Gold is currently holding a critical support level near $5,000 (~ ₹156,000), which remains an important technical floor for the market. A decisive break below this level could trigger further downside, with the next key support emerging around $4,850 (~ ₹150,000). Conversely, if prices manage to stabilize and rebound from current levels, gold could regain upward momentum and potentially move toward $5,200 (~ ₹164,000), followed by $5,250 (~ ₹165,000) in the near term).

Silver is also maintaining strong support around $80 (~ ₹254,000). However, a sustained break below this threshold could lead to additional weakness, with prices likely to decline toward $75 (~ ₹242,000) and $70 (~ ₹230,000). On the upside, if buying interest returns and prices recover from current levels, silver may advance toward $90 (~ ₹280,000) and subsequently test $95 (~ ₹290,000).

Disclaimer: This report contains the opinion of the author, which is not to be construed as investment advice. The author, Directors, and otheremployees of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd. and its affiliates cannot be held responsible for the accuracy of the information presented herein or for the results of the positions taken based on the opinions expressed above. The above-mentioned opinions are based on information which is believed to be accurate, and no assurance can be given of the accuracy of the information. The author, directors,other employees and any affiliates of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd cannot be held responsible for any losses intrading. In no event should the content of this research report be construed as an express or implied promise, guarantee or implication by or from Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd., that the reader or client will profit, or the losses can or will be limited in any manner whatsoever. Past results are no indication of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. The information contained in this report is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. We do not offer any sort of portfolio advisory, portfolio management or investment advisory services. The reports are only for information purposes and are not to be construed as investment advice.