{kind=link}

{kind=link}

Gold prices slipped below $4,700 and silver below $80, retracing a portion of last week’s gains after President Trump publicly rejected Iran’s diplomatic response as “TOTALLY UNACCEPTABLE,” keeping inflationary concerns elevated. Tehran had proposed relocating part of its highly enriched uranium stockpile to a third country while refusing to dismantle its nuclear infrastructure — a position Washington found insufficient.

Geopolitical conditions deteriorated further over the weekend, with renewed cross-border attacks threatening to unravel the fragile ceasefire established in early April. US Central Command confirmed that American forces intercepted Iranian strikes and conducted defensive operations, while guided missile destroyers transited the Strait of Hormuz. The US subsequently reported sinking several Iranian vessels in the strait on Monday, as Iran escalated with fresh missile and drone strikes against the UAE. The Strait of Hormuz remains effectively closed, sustaining elevated energy prices and amplifying inflation risk globally.

Persistent inflationary pressure has reinforced expectations that central banks may tighten policy further — a headwind that typically weighs on precious metals. The April NFP report, released May 8, delivered a significant upside surprise: 177,000 jobs added against a consensus of 65,000, though below March’s 185,000, signaling a gradual cooling trajectory. The unemployment rate held at 4.3%. Rate cut expectations have shifted to late 2027 or early 2028, limiting dollar weakness and capping gold’s near-term upside.

On the USDINR front, currency markets were highly volatile, driven by crude oil dynamics. The rupee depreciated to record lows near 95.2 per dollar on May 7 following a 6% crude oil surge after Iran’s military escalation and a strike on a UAE oil facility. The move constrained capital inflows and triggered a surge in importer hedging activity. India’s physical gold demand has weakened sharply. Imports declined from approximately 100 tonnes in January to 65–66 tonnes in February, fell further to 20–22 tonnes in March, and are estimated at just 15 tonnes in April — among the lowest monthly readings in decades outside the Covid period.

Sentiment last week reflected a tug-of-war between safe-haven demand and the hawkish overlay from elevated energy prices. Analytically, the most notable shift in the pre-NFP environment is a structural repricing of gold: the metal has transitioned from a data-reactive asset to one driven by fiscal sustainability, monetary policy credibility, and sovereign reserve allocation. While Fed hawkishness remains a short-term constraint, 2026 has been defined by what analysts are calling “The Great Bullion Pivot” — gold increasingly rivaling US Treasuries as a preferred reserve asset for central banks globally, for the first time in decades.

Gold has been trading within a $4,500–$4,750 range (approximately ₹148K–₹154K). Having tested the upper boundary last week, profit-booking pressure may push prices back toward the lower end this week. Silver has been ranging between $71–$82 (approximately ₹235K–₹265K), and similarly, having touched the top of its range, a reversion toward support levels is likely in the near term.

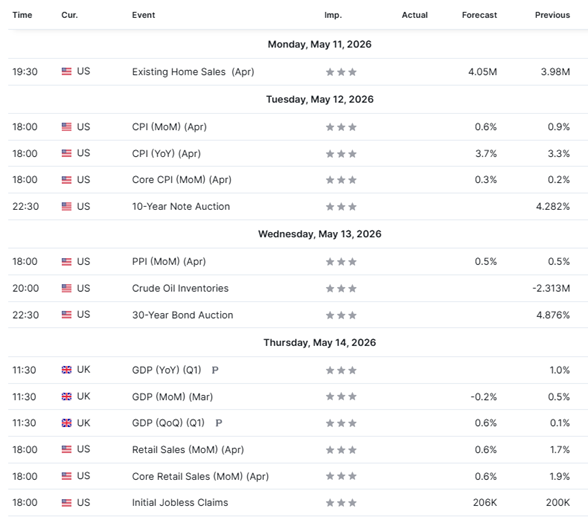

Economic data this week

Disclaimer: This report contains the opinion of the author, which is not to be construed as investment advice. The author, Directors, and other employees of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Ltd. and its affiliates cannot be held responsible for the accuracy of the information presented herein or for the results of the positions taken based on the opinions expressed above. The above-mentioned opinions are based on information which is believed to be accurate, and no assurance can be given of the accuracy of the information. The author, directors, other employees and any affiliates of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Ltd cannot be held responsible for any losses in trading. In no event should the content of this research report be construed as an express or implied promise, guarantee or implication by or from Augmont Goldtech Pvt. Ltd; Augmont Enterprise Ltd., that the reader or client will profit, or the losses can or will be limited in any manner whatsoever. Past results are no indication of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. The information contained in this report is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. We do not offer any sort of portfolio advisory, portfolio management or investment advisory services. The reports are only for information purposes and are not to be construed as investment advice.