{kind=link}

{kind=link}

Gold and silver lost ground last week, giving up their brief rebound as renewed US-Iran military strikes stirred fresh inflation worries and pushed up the odds of another Fed rate hike.

The week’s big story was a renewed flare-up between the US and Iran. After a quiet start on Monday, things escalated on Tuesday when Iran’s Revolutionary Guard reportedly attacked a ship near the Strait of Hormuz, prompting President Trump to warn the US would either strike a deal or “finish the job.” The US responded by revoking Iran’s oil – export license, reimposing sanctions, and striking Iranian air defences, sending oil prices up more than 5% while gold slipped around 1.5%. Gold kept sliding into Wednesday after Trump said the ceasefire deal was essentially dead and even raised the idea of targeting Kharg Island. Sentiment shifted by Thursday, though the dollar softened, stock markets rallied, both sides paused their strikes, and reports pointed to diplomacy still being on the table. That combination helped gold bounce back over 1%, clawing back some losses and settling near $4,100 by Friday.

However, tensions reignited over the weekend. The US carried out fresh strikes on Iranian military targets on Sunday, and Iranian forces fired on commercial vessels moving through the Strait of Hormuz, deepening the standoff over control of this critical waterway. Oil prices jumped about 4%, the dollar strengthened, and Asian shares slipped as the conflict intensified. Gold fell over 1% and silver nearly 2% on Monday, as fears of a Hormuz shutdown pushed oil sharply higher and revived expectations that interest rates would need to stay elevated to fight inflation. However, minutes from the Fed’s June meeting, released last mid-week, showed a divided committee a few members pushed for a rate hike even though the group ultimately held rates steady. New York Fed President John Williams flagged AI-driven

demand as a growing inflation risk, while Fed Chair Kevin Warsh announced five new task forces to review the central bank’s policy approach. Markets responded by raising September rate-hike odds to around 62-64%, up from about 57% the week before.

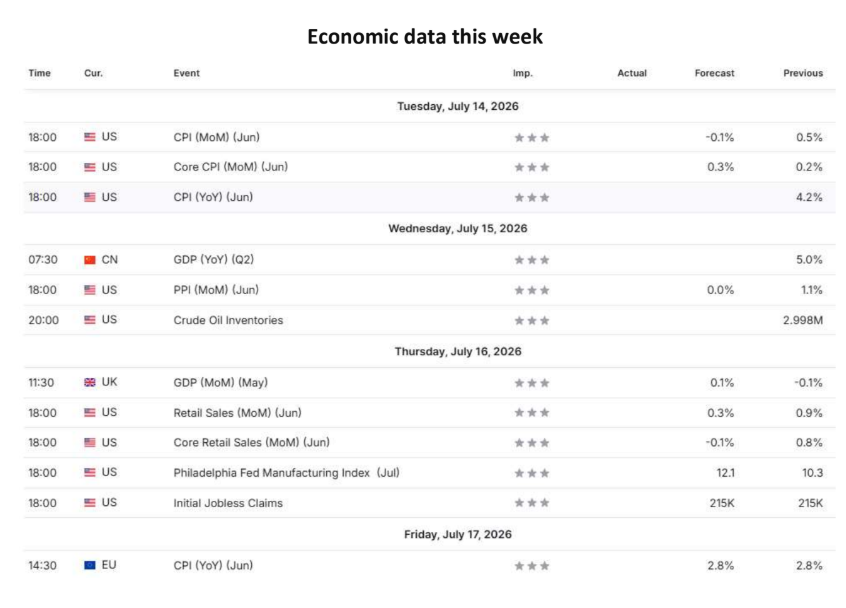

China’s central bank added 14.93 tonnes of gold in June, its largest single-month purchase since 2023 and 20th consecutive month of buying, extending a streak the World Gold Council views as long-term reserve diversification rather than a bet on near- term prices. Globally, 89% of central banks surveyed by the WGC expect official reserves to keep growing over the next year. Attention now turns to Tuesday’s June CPI report, with markets expecting a mild 0.1% dip after May’s 0.5% jump. A hotter print could stoke inflation fears and pressure gold, while a softer one could offer support though the reaction may not last, since investors are also watching Fed Chair Warsh’s Congressional testimony Tuesday and Wednesday. Warsh has already made clear he’s uncomfortable with inflation staying above 2% and isn’t a fan of forward guidance, so a clear signal on rate timing seems unlikely. Markets currently price in roughly a 20% chance of a July hike and about 60% odds of one in September.

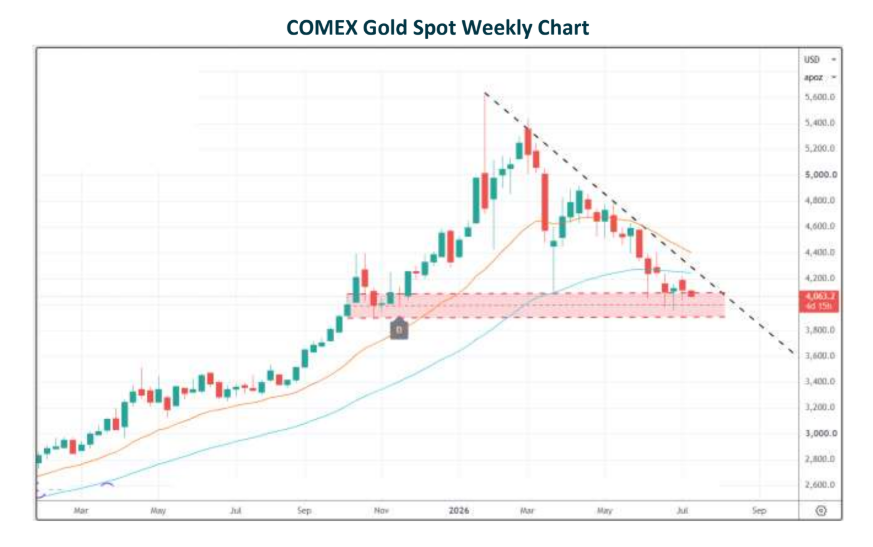

Gold’s next move depends heavily on how the US-Iran situation unfolds. Holding above $4,135 (~ ₹1,45,000) could open the door to $4,200 (~ ₹1,48,000) and $4300 (~₹1,52,000), while a slip below $4,030 (~ ₹1,41,000) risks a deeper pullback toward $3950

(~ ₹1,39,000) and $3900 (~ ₹1,37,500)

Silver remains stuck in a no-trade zone. A sustained move above $63 (~ ₹2,30,000) could push it toward $70–71 (~ ₹2,51,000–2,55,000), while a break below $58 (~ ₹2,20,000) could drag it down toward $55 (~ ₹2,10,000) and even $50 (~ ₹2,00,000).