{kind=link}

{kind=link}

Gold ended flat and Silver rose around 3.5% during the week as the delayed September PCE largely met expectations and the preliminary University of Michigan survey showed easing inflation expectations, a combination that reinforced market conviction in a near term Fed cut.

Headline PCE increased by 0.3% month on month and 2.8% year on year, while core PCE fell to 2.8% from 2.9%, indicating a cooling of underlying pressure. The delayed September PCE and the University of Michigan survey left the prospects of a near-term Fed cut unchanged and reduced one-year inflation predictions, making non-yielding metals more appealing. Combined with ADP’s surprising 32,000 decrease in private payrolls and Challenger’s 71,321 announced layoffs, these data increased the probability of imminent easing, caused position revisions following earlier profit taking, and helped strengthen bullion.

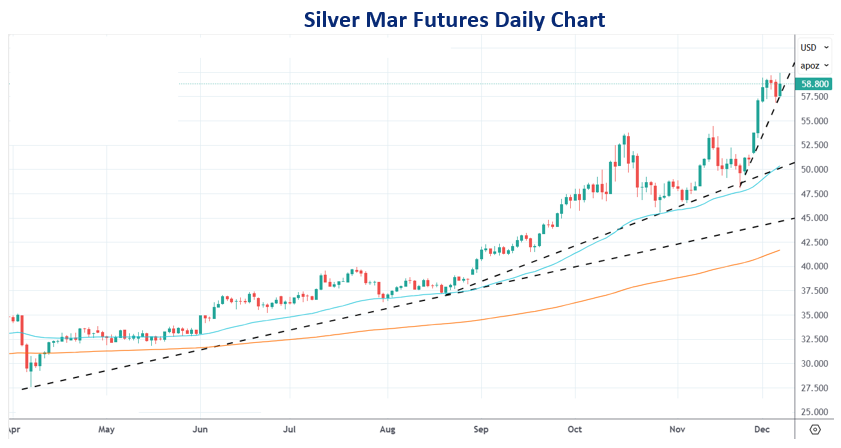

On November 1, Beijing reduced the value-added tax exemption for certain gold purchases made through the Shanghai Gold Exchange and the Shanghai Futures Exchange, which is projected to raise the cost of jewellery and industrial gold. Silver continues to rise, reaching $60, as structural factors underpin the recovery, with low visible exchange inventories, renewed ETF accumulation, and industry estimates of a 2025 supply deficit tightening the market and magnifying short covering, while durable industrial demand from solar and other green technologies supports the medium-term case for higher prices.

Last week, USDINR surpassed the 90 level on concerns over declining dollar inflows into the economy. Meanwhile, the RBI lowered rates by 25 basis points on Friday, leaving room for additional easing. They accompanied the move with a $5 billion dollar/rupee swap to increase rupee liquidity. In February and March 2025, the central bank announced similar buy/sell swaps worth $10 billion over three years. If a trade agreement is not concluded soon, the rupee could go as low as 92 per dollar.

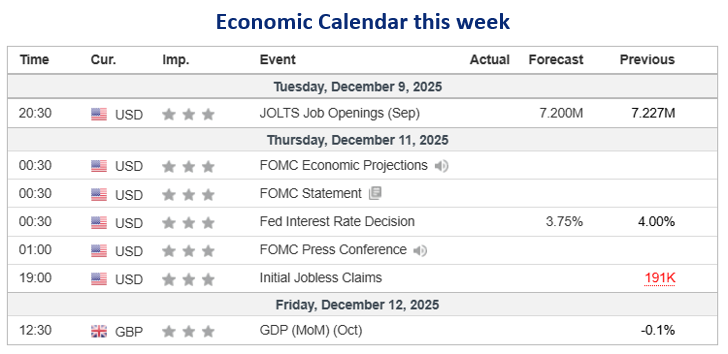

On Wednesday, the focus will be on the FED meeting and dot plot rhetoric. In September, the dot plot forecast three rate cuts by the end of 2026, one more than in June. With the market presently pricing in 63 basis points of easing in 2026, there is a good likelihood that the Fed will lower rates three times next year, making this the baseline scenario. With the 87% possibility of a rate drop already incorporated into pricing, it is expected that gold prices will gain from declines in real bond yields, which will improve gold’s attractiveness in comparison to alternative investments.

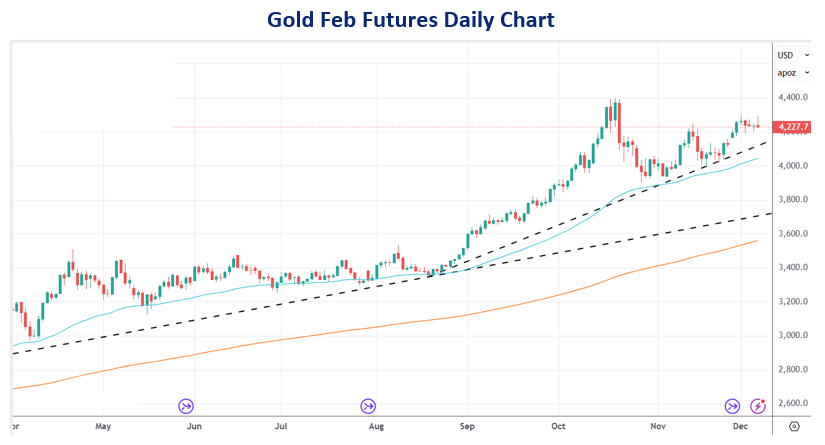

Gold has started its upward journey again; the next target is $4300 (~Rs 132,000) and $4345 (~Rs 133,500) with strong support at $4200 (~Rs 129,000).

Silver can continue its rally towards $60 (~Rs 185,500) and $62 (~Rs 191,000), with firm support at $57 (~Rs 177,000), if tight supply conditions continue.

Disclaimer: This report contains the opinion of the author, which is not to be construed as investment advice. The author, Directors, and other employees of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd. and its affiliates cannot be held responsible for the accuracy of the information presented herein or for the results of the positions taken based on the opinions expressed above. The above-mentioned opinions are based on information which is believed to be accurate, and no assurance can be given of the accuracy of the information. The author, directors, other employees and any affiliates of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd cannot be held responsible for any losses in trading. In no event should the content of this research report be construed as an express or implied promise, guarantee or implication by or from Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd., that the reader or client will profit, or the losses can or will be limited in any manner whatsoever. Past results are no indication of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. The information contained in this report is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. We do not offer any sort of portfolio advisory, portfolio management or investment advisory services. The reports are only for information purposes and are not to be construed as investment advice.