{kind=link}

{kind=link}

Escalating tensions in the Middle East are once again testing investor sentiment, as markets struggle to assess how long the Iran conflict could last and what its broader economic consequences might be. Traditionally, investors turn to safe-haven assets during such periods of uncertainty. However, the current market reaction has been far more nuanced, with some defensive assets rising while others are underperforming. In an environment where even safe havens are volatile, investors are increasingly questioning where capital should be allocated.

Despite its reputation as a crisis hedge, gold declined nearly 3% last week, while silver dropped close to 10%, reflecting the complex dynamics currently shaping global markets. At first glance, the decline may appear counterintuitive since gold historically benefits from geopolitical stress. However, what markets are witnessing resembles classic crisis-driven trading behaviour. During periods of heightened uncertainty, investors often sell liquid assets to raise cash, meet margin calls, or reduce overall risk exposure. Since both gold and silver had rallied strongly earlier this year, they became natural candidates for profit booking.

Rate Expectations and Energy Markets Dominate the Narrative

Another key factor influencing precious metals is the shift in interest-rate expectations in the United States. The ongoing conflict has pushed energy prices higher, raising concerns about a potential inflationary spike. As a result, markets are beginning to scale back expectations for near-term interest rate cuts by the Federal Reserve.

According to CME’s FedWatch Tool, the probability that the Federal Reserve will hold interest rates steady at its June meeting has risen to around 69%, up from 43% just a week earlier, before the conflict escalated. Higher interest rates typically act as a headwind for gold because they increase the opportunity cost of holding non-yielding assets.

In this particular crisis, markets appear to be expressing geopolitical risk more directly through energy prices rather than through gold. Oil markets are responding immediately to concerns over supply disruptions in the region, particularly given the strategic importance of shipping routes such as the Strait of Hormuz.

Rising Military Escalation Adds to Global Risk

Meanwhile, the geopolitical backdrop continues to intensify. Israeli officials have indicated that the military campaign against Iran is moving into its “next phase,” while U.S. Defence Secretary Pete Hegseth recently stated that American military firepower in the region is expected to increase significantly. Britain’s decision to allow U.S. forces to use its bases has further signalled a widening international involvement.

However, unlike earlier global crises, many of the broader uncertainties that historically drove investors toward gold—such as trade wars, tariff shocks, or political instability—are not currently impacting all markets simultaneously. As a result, the energy market has become the primary channel through which investors are pricing geopolitical risk, reducing the immediate need for a generalized hedge like gold.

Physical Gold Demand Softens in Key Markets

In the physical market, demand dynamics are also contributing to price pressure. Traders are reportedly offering discounts of up to $30 per ounce below the London benchmark, as buyers hesitate to place fresh orders amid rising shipping and insurance costs linked to the regional conflict. Disruptions in shipments from Dubai have also affected buyers in India.

Additionally, domestic demand has remained relatively subdued because inventories are already elevated following heavy imports earlier in the year, particularly in January. This temporary oversupply has further dampened near-term buying interest.

U.S. Economic Signals Add Another Layer of Complexity

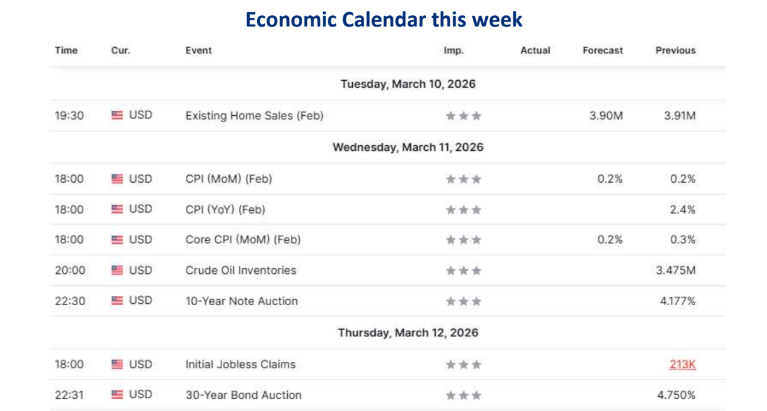

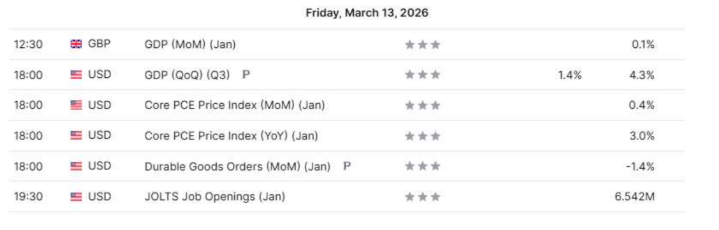

Economic data from the United States has added another dimension to market expectations. The U.S. economy unexpectedly lost 92,000 jobs in February, whereas economists had anticipated a gain of around 50,000. In theory, weaker labour data could strengthen the case for Federal Reserve rate cuts, which would normally support gold prices.

Gold initially reacted positively to the data, briefly rising before retreating from session highs. However, the inflationary impact of rising oil prices has complicated the outlook for monetary easing. As a result, safe-haven demand for precious metals has only partially offset the pressures coming from a stronger U.S. dollar and rising Treasury yields.

Market Volatility Remains Contained

Despite the geopolitical escalation, broader financial market stress indicators remain relatively contained. Key derivatives indicators such as cross-currency basis swaps, swap spreads, and high-yield bond indexes—which often signal liquidity stress—have remained largely stable.

This contrasts sharply with previous crises. Similar indicators spiked dramatically during the 2023 regional banking crisis, the onset of the COVID-19 pandemic in 2020, and Russia’s invasion of Ukraine, when investors aggressively moved into cash.

While some volatility measures have risen this week, the moves have been relatively modest. The VIX index, which tracks equity market volatility, has climbed above 20 after posting its largest weekly increase since last November. However, this remains far below extreme crisis levels, such as when the index surged to nearly 60 during last year’s major tariff-driven market turmoil.

A Crisis Without Full Market Panic

Taken together, the current environment reflects a market that is uncertain but not panicked. Investors are closely monitoring geopolitical developments, energy prices, and monetary policy expectations, but financial markets have not yet entered a full-scale risk-off mode.

For now, the response suggests that while geopolitical tensions remain a significant risk factor, investors are balancing those concerns with broader macroeconomic forces—particularly interest rates, inflation, and liquidity conditions. In such an environment, even traditional safe havens like gold may experience short-term volatility as markets navigate an increasingly complex global landscape.

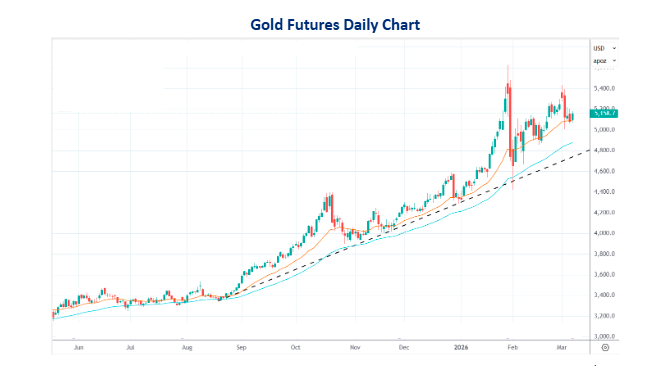

Gold continues to maintain a bullish bias, with prices expected to move towards $5250 (~ ₹165,000) and $5300 (~ ₹167,000) in the near term. Strong support is seen around the $5000 (~ ₹158,000) level, which is likely to act as a key buying zone on any corrective dips.

Gold continues to maintain a bullish bias, with prices expected to move towards $5250 (~ ₹165,000) and $5300 (~ ₹167,000) in the near term. Strong support is seen around the $5000 (~ ₹158,000) level, which is likely to act as a key buying zone on any corrective dips.

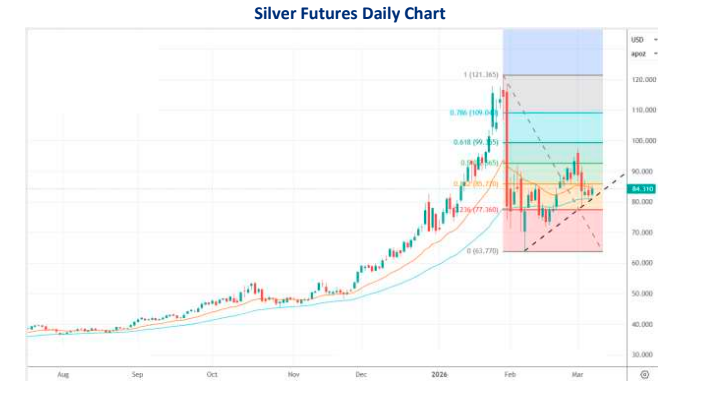

Silver also remains firmly supported and is continuing its upward momentum, with the next upside target seen around $90 (~ ₹282,000). On the downside, strong support is placed near $80 (~ ₹255,000), suggesting that any short-term corrections could attract fresh buying interest.

Disclaimer: This report contains the opinion of the author, which is not to be construed as investment advice. The author, Directors, and other employees of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd. and its affiliates cannot be held responsible for the accuracy of the information presented herein or for the results of the positions taken based on the opinions expressed above. The above-mentioned opinions are based on information which is believed to be accurate, and no assurance can be given of the accuracy of the information. The author, directors, other employees and any affiliates of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd cannot be held responsible for any losses in trading. In no event should the content of this research report be construed as an express or implied promise, guarantee or implication by or from Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd., that the reader or client will profit, or the losses can or will be limited in any manner whatsoever. Past results are no indication of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. The information contained in this report is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. We do not offer any sort of portfolio advisory, portfolio management or investment advisory services. The reports are only for information purposes and are not to be construed as investment advice.