{kind=link}

{kind=link}

Silver plummeted 8% last week, from a high of more than $82 to around $70. Gold also plunged, plunging 5% from $4580 to $4300 as the CME upped the first margin twice last week. The CME increased the initial margin and maintenance cost by 47% for non-speculators and 55% for speculators compared to the pre-December condition.

Silver surged over 6% to $76, while gold rose beyond $4400 on Monday, extending gains after the US bombed Venezuela and captured President Nicolas Maduro over the weekend, raising geopolitical concerns and increasing demand for safe-haven commodities. President Trump stated on Saturday that the US will “run” Venezuela until a legitimate political transition occurs, while Secretary of State Marco Rubio indicated that Washington has leverage to achieve its goals without personally managing the country.

Despite the recent dip, gold and silver remain in a longer-term uptrend. The decline was fuelled by margin increases, tight liquidity, and renewed volatility, but the underlying fundamentals continue to support rising prices. The Federal Reserve’s rate cuts and indications of more easing into 2026 lower the opportunity cost of owning gold, but persisting geopolitical concerns maintain safe-haven demand high.

Increased geopolitical tensions across many global flashpoints have bolstered gold and silver’s status as preferred safe-haven investments. Escalating tensions between the United States and Iran, fresh strains in US-Venezuela relations, and the ongoing Russia-Ukraine conflict have all contributed to greater uncertainty in bullion markets, global commerce and financial stability.

Silver’s ascent has been structurally supported by governmental measures at both ends of the global supply chain. In November, the United States identified silver as a key mineral due to its applications in electrical circuits, batteries, solar cells, and anti-bacterial medical tools. The United States’ decision to include silver on its important minerals list has increased the metal’s strategic relevance, encouraging long-term investment and policy-backed demand.

At the same time, China’s move to restrict silver exports through stricter licensing has heightened supply concerns, given its leading role in global production and refining. The combination of increased strategic demand and tight supply has elevated silver from a purely cyclical commodity to a strategic asset, resulting in substantial price gains.

The new rules will replace a quota system that has been in force since 2000. Under the harsher system, exporters must fulfil stringent standards: businesses must demonstrate that they exported silver annually from 2022 to 2024, while new applicants must demonstrate annual production of more than 80 tons and continuous export records.

China exported more than 4,600 tons of silver in the first 11 months of the year, greatly exceeding the roughly 220 tons imported during that time. The exact amount that China will export in 2026 is unknown, although 44 companies have been granted a license to export silver from 2026 to 2027, indicating a regulated supply. This measure is part of a push for stricter controls over vital minerals.

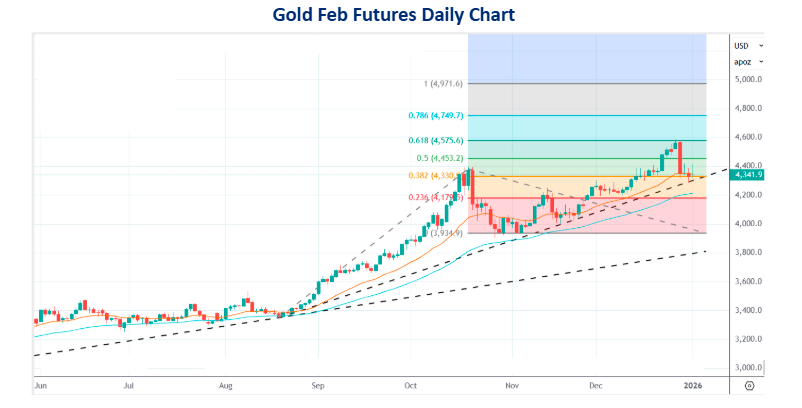

The recent rally in gold began around $3400 in August 2025 and reached $4400 in October 2025. The advance then retraced 50% to $3900 before extending again by 61.8% to $4580 in December 2025. Further Fibonacci extension suggests that $4750 and $4970 will be significant resistance in the next months in 2026. Strong support lies around $4300.

If the Silver rally started from $45 in October, and extended up $82.7 in December 2025. Fibonacci extension suggests that this rally can extend further towards $88.60, $99 and $107 in the coming few months of 2026. Strong support lies at $64.

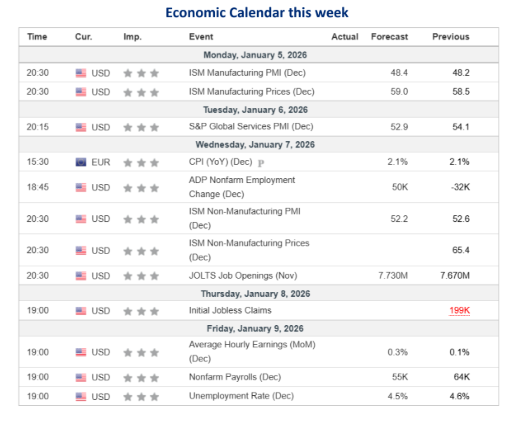

The US jobs report will be the main economic release this week, with other US data including the ISM indices and consumer sentiment. Elsewhere, the focus will be on inflation in Europe and China.

Disclaimer: This report contains the opinion of the author, which is not to be construed as investment advice. The author, Directors, and other employees of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd. and its affiliates cannot be held responsible for the accuracy of the information presented herein or for the results of the positions taken based on the opinions expressed above. The above-mentioned opinions are based on information which is believed to be accurate, and no assurance can be given of the accuracy of the information. The author, directors, other employees and any affiliates of Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd cannot be held responsible for any losses in trading. In no event should the content of this research report be construed as an express or implied promise, guarantee or implication by or from Augmont Goldtech Pvt. Ltd; Augmont Enterprise Private Ltd., that the reader or client will profit, or the losses can or will be limited in any manner whatsoever. Past results are no indication of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. The information contained in this report is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. We do not offer any sort of portfolio advisory, portfolio management or investment advisory services. The reports are only for information purposes and are not to be construed as investment advice.